Whether you’re just thinking about buying a home or are already preparing for closing day, it’s helpful to know exactly what you need as a buyer before you close on your home.

At The Home Loan Expert, we’re passionate about making the home loan and closing process simple and accessible from our 10-day closing guarantee to creating a buyer’s guide to closing day! Let’s dive in.

How to prepare for closing day: a buyer’s checklist

Ready to close on your home? This is what you need to know and do to prepare for closing day.

Get a Home Inspection

When you made an offer on the house, you likely included an inspection or due diligence contingency clause. These contingencies allow you to inspect the property for potential damage before purchase.

If something comes up during the inspection, such as costly repairs, you can cancel the sale within a specified time.

Mortgage lenders will require you to get a professional home inspection. Your realtor will likely be able to recommend a third-party inspector who will carefully examine the roof, foundation, HVAC systems, windows, doors, ceilings, insulation, and other structural components of the home.

If there is any damage in the home, you have the option to negotiate repairs or the property price with the seller.

Prepare for Closing Costs

Mortgage closing costs can add up, so it’s imperative to know what you’re liable for. Some common examples may include title insurance and transfer, property tax, attorney, HOA, and mortgage costs.

In most cases, the buyer will be responsible for more part of the closing costs than the seller. While sellers usually have to pay taxes and some fees, the buyer has additional expenses due at closing, like the home appraisal and inspection and a property title search.

Before closing, you’ll also need to have your down payment ready. The typical down payment on a home is 20%. This is in addition to any closing fees you may have. Your lender can help outline the specific expenses you will have. While all this can add up, in the long term the cost of home mortgages are often less than renting.

Be sure to bring any escrow account information, proof of wire transfers, or checks to closing. While some lenders may accept cash, it is always better to have a physical paper trail.

Review the Closing Disclosures

Prior to closing, the buyer must carefully review their mortgage agreement and the closing disclosures. These documents will detail your expected monthly payments, the loan length, and the interest rate.

If your lender expects you to pay any additional fees, they will outline them in the closing disclosure. If you need any of the details explained, contact your lender before closing to avoid surprises.

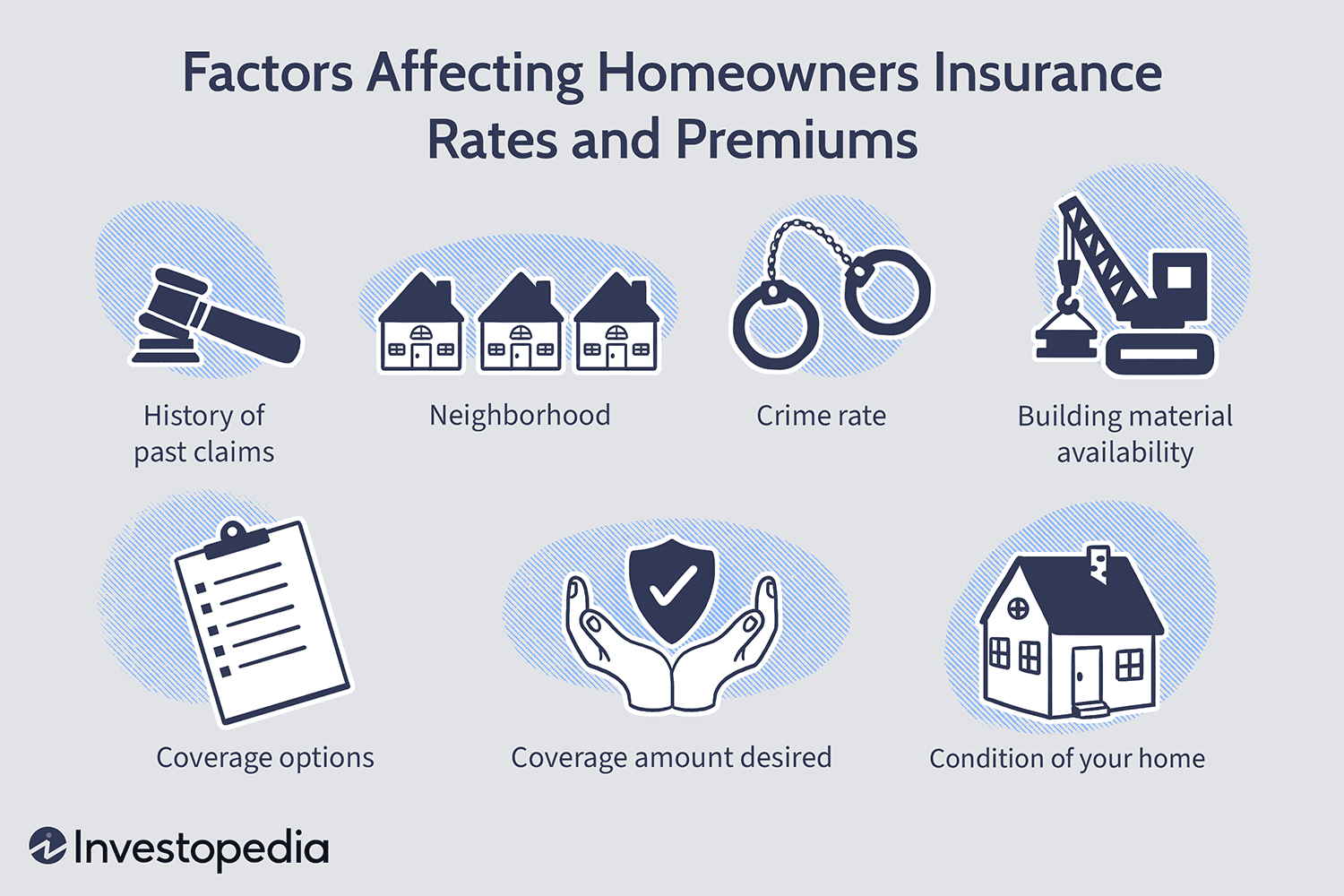

Select Your Homeowners Insurance Provider

Your lender will require you to have homeowners’ insurance before closing the sale to help protect you and your lender in the event of damage. Every lender will have different requirements, but selecting the most accommodative policy is essential.

Typical coverage can include a combination of personal property, dwelling, personal liability, and living expenses coverage. Add-ons, such as flood and earthquake insurance, are also recommended.

Consider each policy carefully when buying homeowners insurance. The providers you have available will vary greatly depending on your location. Your lender will be able to help you find local providers.

Hire a Real Estate Lawyer

Having professional representation is always a good idea when you’re closing on a home. Real estate lawyers help to ensure all of your paperwork is in order prior to closing. They will also likely attend the closing.

According to our First Time Home Buyer Checklist, your realtor should be able to suggest a real estate attorney. Be sure to read reviews and research the attorney before hiring them.

Gather Necessary Documents

While a real estate lawyer will review documents to ensure everything is in order prior to the sale, you will likely need to bring some documentation to the closing. Ask your lender and real estate agent if any additional loan documents are required for the sale to be final.

Some common examples include:

- Proof of homeowners insurance

- A copy of your loan application

- A certificate of occupancy

- Government-issued photo identification

- Loan application

- Property deed

- Bill of sale

- Mortgage note

Your lender may also request additional documentation before closing.

Complete any lender requests

Every real estate sale is a little different. If your lender needed anything prior to closing day on a home, they likely would ask beforehand, but it isn’t uncommon for requests to come up last minute.

Make sure to frequently check your email, voice messages, and texts and promptly address any last-minute requests. This will help you avoid delays on closing and getting your dream home!

Do a Final Walkthrough

The final step before signing any paperwork is to complete a walkthrough. This is a simple and brief process that allows the buyer to confirm that the property’s condition hasn’t changed before closing. Most final walkthroughs will occur 24 hours before closing.

Double-check to ensure that any negotiated contingencies or repairs are complete and satisfactory.

What to Expect on Closing Day as a Buyer

Closing day on a new home can make anyone nervous. After the long journey of searching, negotiating, and securing a mortgage, everything hinges on this moment. But what exactly does it entail?

In short, your primary responsibility at a closing is the signing of important legal documents, paying closing costs, and completing the walkthrough. These documents outline your agreement between you and your mortgage lender, and between you and the seller of the property.

As a first-time home buyer, you may have a lot of questions about your new home. Here are some common frequently asked questions.

How long does it take to close on a house?

According to Zillow, closing mortgages can take as long as 52 days. This number can vary greatly depending on several factors.

With a pre-approval from The Home Loan Expert, you ‘ll be backed by our 10-Day Closing Guarantee*. While other lenders are taking months to close, we know that an on-time closing matters. And because we use the most streamlined digital mortgage technology on the market, we can get you home fast.

So what does the guarantee mean? It means that if we don’t close your conventional loan in 10 days, we’ll give you a $1,000 gift card.

Refinancing? The 10-Day Closing Guarantee* also applies to our most popular refinance option, the cash out refinance. With historic home values, now might be the time to tap into your home’s equity.

On average, our clients are receiving over $54,000 with a simple cash out refinance for debt consolidation or home improvements.

Start your application process at The Home Loan Expert today!

How long does it take to sign closing papers?

After your underwriter and lender have completed their paperwork and the home has been appraised, the rest of the closing process is usually relatively quick. It typically takes less than a day to get homeowner’s and title insurance if you already have a provider in mind.

You’ll likely need to make a closing appointment to sign the paperwork. The appointment can vary in length, but you can sign most paperwork within a few hours or less.

Can you move in on closing day?

Does closing on a house mean you get the keys? Unfortunately, you might not get the keys to your dream home on closing day. In many cases, you will be able to move in as soon as the sale is recorded and the funds have been properly disbursed. Sometimes, this can take a few days to complete.

You’ll also need to review your contract, as some sellers will request a short period of occupancy after the sale, which is often the case if the seller is currently residing in the home and needs time to move their belongings out.

Your real estate agent should be able to estimate how long you will need to wait after signing the paperwork to get the keys to your new home..

What closing documents do buyers need to bring?

Your lender should review everything you need before closing day. Typically, you will need a government-issued ID for the title company to verify your identity, a cashier’s check to cover any closing costs you are responsible for, your down payment, the closing disclosure, and proof of insurance.

You should make sure to get the cashier’s check a few days before closing so you have some cushion if there are any delays at the bank.

If you’re missing any of these documents, you won’t be able to sign the closing paperwork so use this checklist for buyers as a reminder!

My mortgage fell through on closing day…what do I do?

Due to finance changes, inspection issues, or title or deed changes, mortgages can fall through on closing day. If this happens, you have a few options:

- Add more to your down payment, so the amount you’re borrowing is less

- Try to find another home you’re as excited about. Though this can be disappointing, if you need to find a home soon this could be a good option.

- Take some time from the home buying process to improve your finances.

- Find a new lender. A new lender can give you more favorable terms or rates that can help you see the closing through. Contact the The Home Loan Expert today to get your home closed in 10 days or less.

What to Do After You Close on Your House

After you close on your new house and have your keys, there are a few things you need to do to get ready for move-in:

- Replace the locks on all doors and install a security system.

- Turn on or change billing for any utilities.

- Clean your home from top to bottom.

- Make any necessary repairs that the seller wasn’t required to make.

- Check, install, or replace carbon monoxide and smoke detectors as needed.

What Not to Do After Closing on a House

There are a few things homeowners should avoid doing during and after signing. During the closing process, you should avoid changing jobs, switching banks, and making large purchases, as these could affect lending.

Here are some additional suggestions:

- Don’t hire a moving company or rent a truck for the same time as your closing.

- Don’t furnish everything with credit cards or add a lot of household debt right away.

- Don’t forget to change your address with your local post office.

- Don’t post your home on social media right away, especially if you don’t have a security system yet.

- Don’t forget to verify that all utilities are in your name.

- Don’t be afraid to ask your real estate agent, lawyer, or lender any additional questions.

Get to Closing Day Quicker with The Home Loan Expert

Buying a home can be complicated; however, if you have the right team by your side, you won’t have to worry. The Home Loan Expert helps to streamline the lending process for buyers, starting with a quick online pre-approval process.

The Home Loan Expert strives to make buying or refinancing a home simple. For example, conventional purchases can take over a month to complete, but The Home Loan Expert’s 10-day closing guarantee means you get to move quickly in this current market.

Contact the The Home Loan Expert today to get your home closed in 10 days or less!

Glide Support

Glide Support