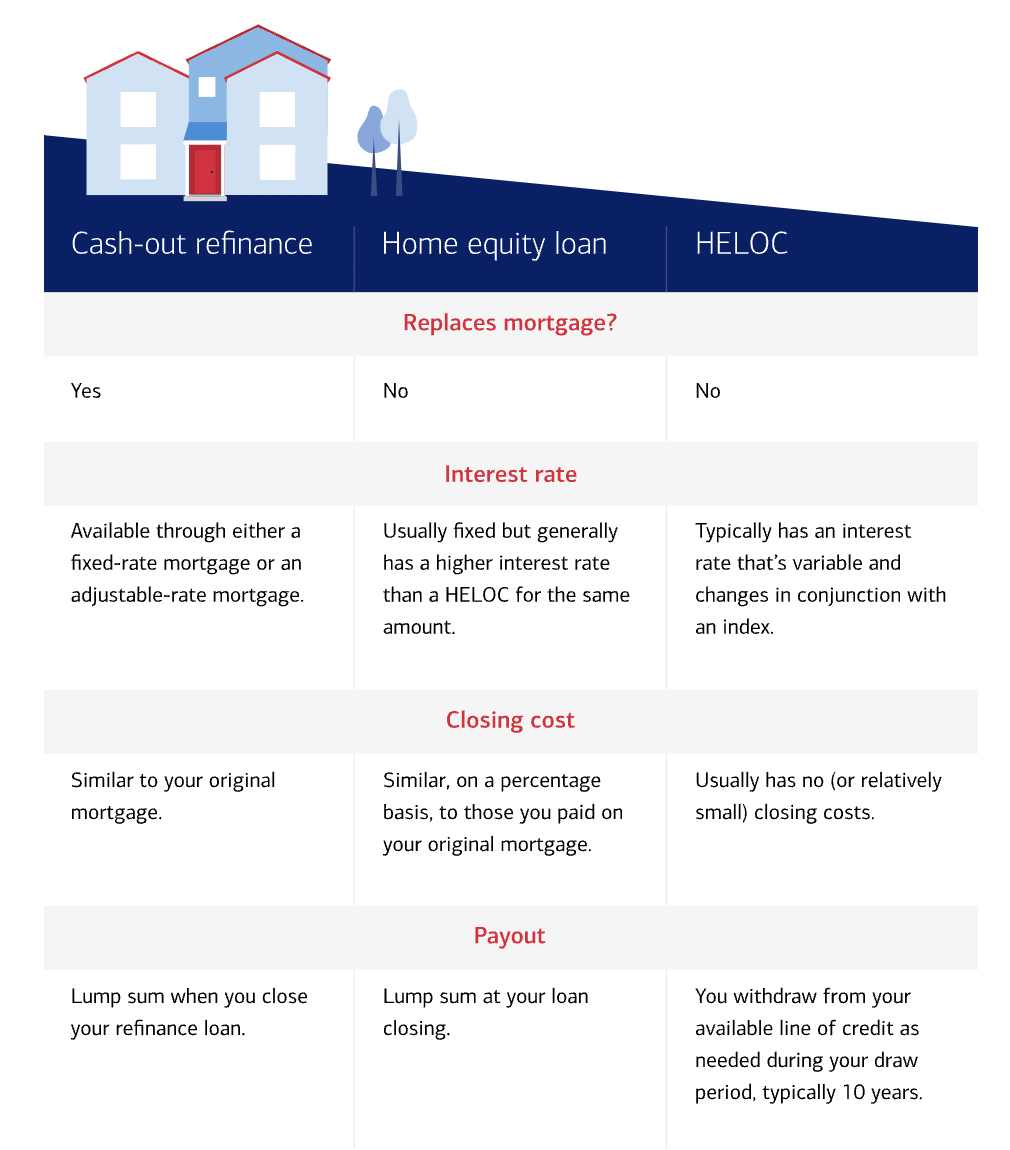

There are a few different ways for you to acquire funds through your existing home. Two of the most popular are cash-out refinancing and home equity line of credit.

Each of these has its own set of pros and cons that will determine which type of home equity opportunity will serve you best.

In this article, we will be doing a full dive into the differences between a cash-out refinance vs. HELOC and which option is best for you.

What is Cash Out Refinance?

Cash-out refinances are a type of mortgage refinance that allows you to take advantage of the equity you’ve already built. In turn, it gives you cash as a result of you taking a larger mortgage than your original. Basically, you’re able to borrow more than what you typically owe on your mortgage and keep the difference.

Compared to taking on a second mortgage, cash-out refinances don’t add additional monthly payments to your bills. You pay out your old mortgage through the cash-out refinance loan, and then have different monthly payments.

Let’s say you’ve purchased your new home for $300,000 and have paid $80,000 since your purchase. That leaves you with $220,000 that you still owe. And maybe you want to pay off your student debt of $30,000.

In this scenario, cash-out refinance loans allow you to take a portion of your equity and add what you want to take out to the new mortgage. In the end, your new mortgage would be valued at $250,000 ($220,000 that you originally owe + the $30,000 for your student debt). Plus, any additional fees included in the closing costs.

You aren’t restricted with what you would do with the money you take out from your own equity. A student loan is just one example of what you would typically do with a refinance, but you can also use the cash for home improvement, other debts, and other upcoming expenses.

What is HELOC (Home Equity Line of Credit)?

A home equity line of credit (HELOC) is a type of second mortgage that would allow you to borrow money against the equity you’ve already built into your current home. Similar to credit cards, you’re able to access these funds and then pay them off later. These untapped funds don’t require any additional interest charges.

However, HELOC is basically a second mortgage. This means you’re paying for an additional monthly mortgage because it is considered an additional loan to your property.

Another thing to consider is that with a HELOC is that there are different periods for borrowing and repayment. You can only use the line of credit during your draw period.

Once this period ends, you’ll lose your ability to access the HELOC funds and will have to start making full monthly payments that would cover the principal balance with interest. This is the repayment period.

Cash-out Refi vs Home Equity Line of Credit

If you’re wondering whether or not a cash-out refinance or a HELOC would fit you best, you need to determine how you’re planning to use the equity you’re taking out and the overall amount of home equity you have.

Perhaps the most important thing you need to consider is how much your equity is worth, since this is the basis of how much you can borrow overall.

Cash Out Refinance vs. HELOC Rates

HELOC has a variable interest rate that is dependent on a benchmark interest rate, like the U.S. Prime Rates index. This means that your interest rate can go down–and up–over time.

Cash-out refinance loans allow you to decide if you want a fixed-rate mortgage, or a variable-rate loan.

Which is easier to qualify for? HELOC or Cash-out refinance loans?

In general, cash-out refinances are usually easier to qualify for than a HELOC. This is because you are simply replacing your primary mortgage, while HELOC loans are classified as a second mortgage on top of your original home mortgage. Since you’re paying for two mortgages with HELOC, there is a larger risk for the lender.

While it may usually be easier to qualify for cash-out refinance, it’s best for you to shop around and ask for quotes and requirements regarding each of these options to figure out which suits you best.

Reach out to our friendly team at The Home Loan Expert to discuss refinancing options and rates today!

Cash Out Refinance vs. HELOC Calculators

To see how much you might be able to borrow from your home, these calculators are a good tool for you to measure your equity and your overall capacity when deciding between a cash-out refinance vs. HELOC.

Pros and Cons of Cash Out Refinancing vs. HELOC

Cash-out refinancing and HELOC have their own inherent pros and cons that set both apart from one another. To give a clearer picture here are different advantages and disadvantages you receive when opting for either option.

Home Equity Line of Credit Pros

Interest may be tax-deductible

Depending on how you use the money you get from HELOC, you could deduct the interest from tax if you use the funds for home improvements. According to the IRS, interest payments on home equity products can be deductible only if the funds are used to “buy, build, or substantially improve the taxpayer’s home in a manner that secures the loan.”

Borrow only what you need

Since HELOCs are similar to credit cards, you typically would only take out the money you need—not a lump sum.

Flexibility in making payments

While interest payments will be paid during the draw period, you also have the option to make principal payments over time.

Fewer restrictions on fund use

With the money you borrow from a HELOC, there are little to no restrictions on how you can use the acquired funds. Though it is ideal to use on home improvements, it is not uncommon for individuals to use HELOC funds to pay off education and other debt.

Home Equity Line of Credit Cons

Variable Interest Rate

Since HELOC comes with a variable interest rate, your interest rate can frequently change. Even when you take out a HELOC with a low starting interest, it’s possible to have higher interest rates during your repayment period.

Possibility of Overspending

When applying for a HELOC, it’s important to gauge your own discipline when it comes to managing your own money. Because you have the ability to access cash easily, borrowers that are very impulsive can suffer in the long run.

Your Home is Collateral

There is always added risk when you’re placing your home as collateral, because you risk foreclosure if you’re unable to make your monthly payments.

Cash-Out Refinancing Pros

Low Interest Rates

As a borrower, you’ll ideally pay as little interest as possible when you apply for a large loan. Cash-out refinance allows for this with its lower interest rates.

Improve Credit Score

Taking on cash-out refinances and successfully paying off this debt can potentially increase your credit score in the long run.

Takes Advantage of Tax Deductions

When using your funds for home improvements, you could apply for tax deductions depending on the eligibility requirements from the IRS that your home project meets.

Cash Out Refinancing Cons

Can Pay PMI

While it is possible for lenders to let you withdraw even 90% of your home’s overall equity, doing so might mean you would have to pay for private mortgage insurance. This can add up to your overall borrowing costs if you aren’t careful with maintaining your equity threshold.

Your Home is Collateral

Just like with HELOCs, there is always a risk when you’re placing your home as collateral.

Cash-out Refinance or HELOC: which is better?

So, which is better? It really depends!

To figure out which can benefit you the most, consult with our dedicated team at The Home Loan Expert and get you started on either a cash-out refinance or a HELOC as soon as possible.

Glide Support

Glide Support