Are you a first-time homebuyer in Illinois? Or just need an FHA Loan in Chicago, Indianapolis, or another Illinois city? Here at The Home Loan Expert, we’ve helped many Illinois residents purchase a home with a lower down payment through FHA Loans.

FHA stands for the Federal Housing Administration, a government body that insures mortgage loans for United States residents. The appeal? Lenders can offer lower interest rates and better financing options without the risk, because the government backs them.

Of course, FHA Loan requirements and limits always apply, and Illinois is no different.

What is the FHA?

The FHA is a government agency operating within the U.S. Department of Housing and Urban Development (HUD). The goal of the FHA is to make mortgages accessible and affordable for lower-income and first-time homebuyers, multi-family rental properties, hospitals, and residential care facilities. They do this by insuring the loan, thereby protecting the mortgage lenders from potential losses.

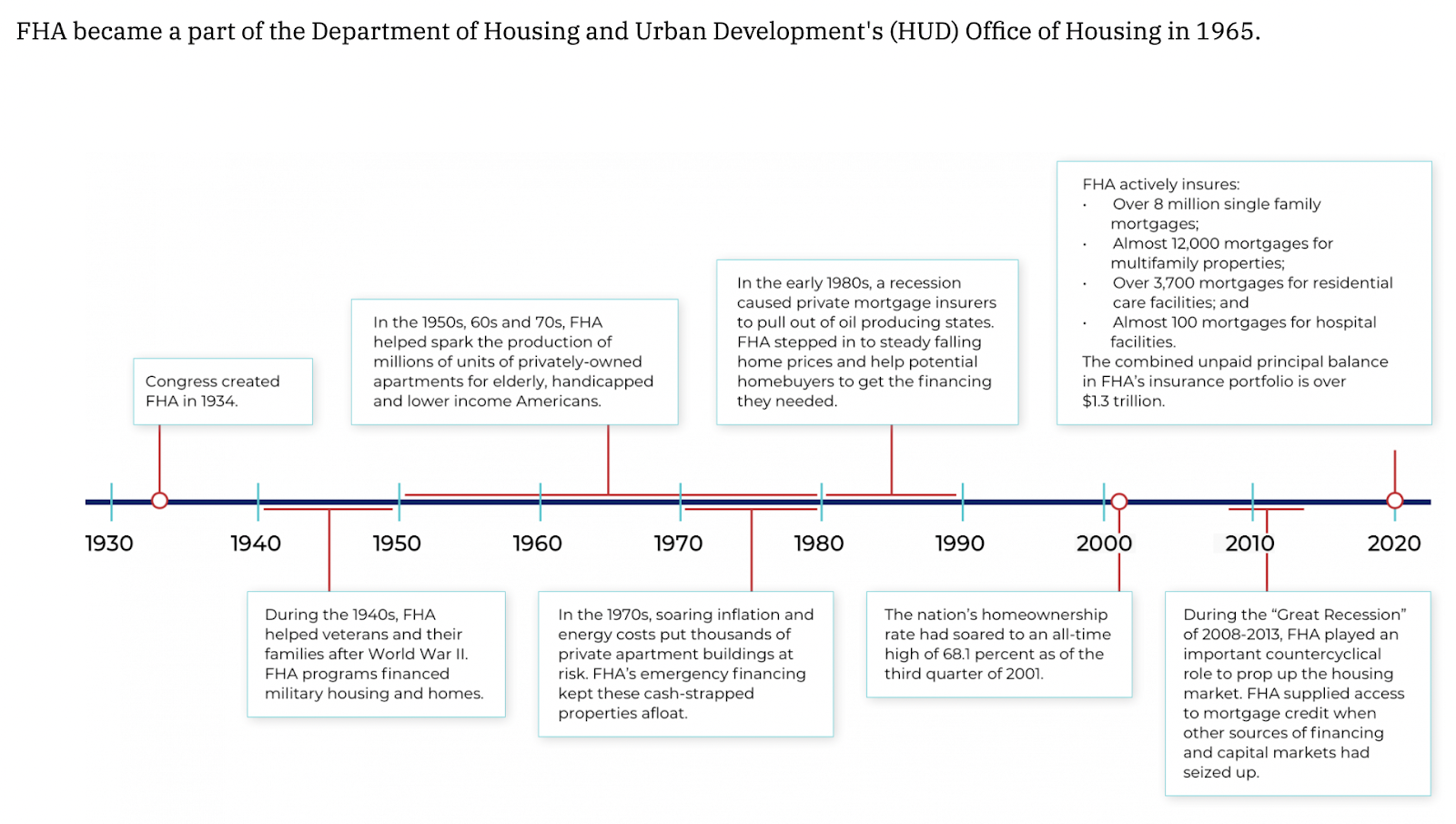

The FHA Loan program traces its roots back to the Great Depression of the 1920’s and was created to give banks insurance protection, and to assist homeowners and new home purchasers when the foreclosure rates and defaults on loans were skyrocketing.

It now operates primarily to help borrowers that can’t afford a down payment, or won’t qualify for private mortgage insurance (PMI). It’s an insurance policy for the bank that guarantees the loan against default.

The Federal Housing Administration was established in 1934 during the Great Depression, when the housing market drastically decreased as a result of the banks failing. Large down payment requirements of 30-50%, and short mortgage periods of five to 10 years meant that home ownership was out of reach for working class families.

Once the FHA was established, and with the granting of FHA-secured loans, down payment requirements went down, and the mortgage lifespan grew to 20-30 years. Since 1934, the FHA has insured over 50 million mortgages throughout the U.S., and is the largest mortgage insurer in the world.

What is an FHA Loan?

A Federal Housing Administration Loan is a loan that is backed by the FHA’s mortgage insurance. It’s a federal program that assists families with moving into a home with the small down payment. The only current FHA requirement to buy a home is a down payment of 3.5 percent.

FHA Loans are mortgages from private lenders that are insured by the government. If you are a first-time homebuyer or have a low to moderate income, an FHA loan may be just what you need to become a homeowner.

Banks and other lenders are willing to work with “higher risk borrowers,” knowing that the Federal Government is backing them. FHA loans have much to offer over conventional loans, such as:

- Lower qualifying credit scores

- Lower down payment requirements with more flexibility regarding the origin of the down payment (personal savings, gift, or even grants).

- Candidates can have a higher debt-to-income ratio

While these benefits make FHA loans appealing, there are some conditions to be aware of:

- FHA loans are only available for certain types of properties

- Some loans may require closing costs that don’t exist with conventional loans

- Every FHA loan requires mortgage insurance built into the loan

- Lenders may have their own rates, fees and approval processes separate to the FHA, so research is needed

- FHA loan limits restrict your borrowing power

We use FHA to offer refinancing as well, with half of our refinancing that we now do is through FHA Loans. They allow the borrower to get a mortgage on up to 97.5 percent of the home’s value instead of topping out at 90-95% for a conventional loan.

Ready for your Illinois FHA Loan? Get started on our 5-minute loan approval application today!

What is the minimum credit score for an FHA loan in Illinois?

The minimum credit score for an FHA loan in Illinois is 580. However, if your credit score is below 580 then the down payment requirement will have to be 10% of the purchase price of the home.

What will disqualify an FHA Loan?

FHA Loans require certain criteria in order for homes to meet the minimum standards for a loan to be approved by a participating lender. Reasons an FHA Loan may be disqualified are:

- Homes must be primarily residential: If the home is not primarily used for residential purposes and has 50% or more floor space is taken up for non-residential use, it cannot qualify for an FHA mortgage.

- Compliance issues and FHA appraisal standards: If a home is in a state of severe repair it may be disqualified for an FHA loan. However, there are FHA Rehabilitation loans for homes that do not pass an appraisal for the typical FHA loan.

- Home may be near certain flood zones without insurance: Certain natural disaster zones do not automatically disqualify a home buyer from an FHA loan. However, if the necessary insurance is not available in the area it may result in disqualification.

- Property is too close to potential hazards: If the home is too close to areas that are considered “potential hazards” like high voltage electrical wires, mining, and high-pressure gas lines, an FHA loan may not be possible.

- Transient occupancy properties are not in compliance: FHA loans cannot be used on homes that will be rented out to individuals that will be staying at the property for less than 30 days. FHA loans cannot be used for bed-and-breakfasts, condo hotels, Airbnbs, and other occasional rentals. situations.

FHA Loans vs. Conventional Loans

FHA loans have much to offer over conventional loans, such as:

- Lower qualifying credit scores

- Lower down payment requirements with more flexibility regarding the origin of the down payment (personal savings, gift, or even grants).

- Candidates can have a higher debt-to-income ratio

While these benefits make FHA loans appealing, there are some conditions to be aware of:

- FHA loans are only available for certain types of properties

- Some loans may require closing costs that don’t exist with conventional loans

- Every FHA loan requires mortgage insurance built into the loan

- Lenders may have their own rates, fees, and approval processes separate from the FHA, so research is needed

- FHA loan limits restrict your borrowing power

Types of FHA Loans

The FHA offers specialized mortgage loans for specific audiences that can help you afford your dream home. Here’s a bit about each one:

Traditional Mortgage Loan: This is a regular mortgage loan that applicants can use for their primary residence.

203(k) Mortgage Program: This is a traditional mortgage with extra money added for home repairs and renovations. If you purchase a home that needs some TLC, this is the loan for you.

FHA Energy-Efficient Mortgage: Interested in making environmentally friendly home upgrades to save energy? This loan includes extra funds to do so. Examples of eligible upgrades include new solar panels or insulation to retain heat.

Home Equity Conversion Mortgage (HECM): If you’re a senior, you might struggle to find retirement options if you don’t have a solid pension plan. The Home Equity Conversion Mortgage (HECM) is a reverse mortgage that offers mortgage payments to the applicant in exchange for equity in their home. You can receive the payments every month or withdraw them at your discretion through a line of credit. You might consider a combination of these two options.

Section 245(a) Loan: Maybe you started a business and need a few months to get the profits flowing. Or, you’re promised a promotion in the next few months at your current corporate job. This Graduated Mortgage Payment (GPM) loan starts with monthly payments at a certain amount that increases over time. You can also opt for the Graduated Equity Mortgage (GEM) loan, which increases monthly principal payments specifically over time to gain more equity in your home faster.

Now that you’re up to speed on FHA Loans, let’s explore the FHA Loan Limits Ohio offers.

What is an FHA Loan Limit?

An FHA Loan limit is the maximum loan amount you can borrow while still having the FHA insure that loan. FHA Loans have been a success for many homeowners, and offer many people greater affordability and access to credit that they otherwise might not be eligible for with a regular bank.

How are FHA Loan Limits Determined?

The FHA determines loan limits based on the region, cost of living, average construction costs, and the average home sale price for a particular area. Every year, the FHA updates the FHA Loan limit depending on changes in all the above factors for different states and counties.

Areas with lower costs have a “floor” limit that is lower than average, while higher-cost areas have a “ceiling” limit that is higher than average. Otherwise, the FHA Loan limit is typically 115% of the median price of a state or city’s average home, provided the amount is before the area’s ceiling and floor limits.

Some regions are considered “special exceptions” where the FHA allows for higher loan limits due to increased construction costs.

What are the FHA Loan Limits in Illinois?

All of the counties in Illinois have the following FHA loan limits:

- Single-family: $420,680

- 2 Units: $538,650

- 3 Units: $651,050

- 4 Units: $809,150

How to Apply for an FHA Loan in Illinois

Individual lenders might have some variations in their FHA Loan requirements, but the basics are the same. Before anything else, you’ll need:

- Valid Social Security number

- Proof of residence in the United States

- Legal age according to your state

After you meet these qualifications, an FHA Loan is easier to obtain than a traditional mortgage. Here are some more specific FHA Loan requirements:

- Minimum credit score: 500

- Loan term length: 15 or 30 years

- Minimum down payment: 3.5% for credit scores over 580; 10% for credit scores between 500-579

- Down payment gift: Entire down payment can be a gift

- Down payment assistance: Programs available

- Mortgage insurance: Upfront and every year for the life of the loan or 11 years

- Mortgage insurance premiums: 1.75% upfront; 0.45%-1.05% annually

If your credit score is less than 500, consider lowering your debt-to-income ratio, setting alarms to avoid late payments, or delaying your mortgage application until your credit score is a bit higher.

Important FHA Loan Terms

As you learn more about FHA Loan requirements, limits, and more, it’s essential to keep track of some standard terms that might pop up. Here are some important FHA Loan terms for your reference:

FHA: Federal Housing Administration

Ceiling: Higher FHA Loan limit than usual for higher-cost living areas

Floor: Lower FHA Loan limit than usual for lower-cost living areas

Mortgage Insurance: Insurance you must pay every month to protect yourself in case you default on loan payments. Having this insurance is often a requirement for many FHA Loans.

203(k) Mortgage Loan: FHA Loan for people that need to make major renovations to their new home

Home Equity Conversion Mortgage: Reverse mortgage FHA Loan for seniors aged 62+

Section 245(a) Loan: Graduated Mortgage Payment (GPM) with increased monthly payments over time; Graduated Equity Payments with increased principal monthly payments over time.

FHA Energy-Efficient Mortgage: FHA Loan that accounts for costs to make energy-efficiency upgrades to a new home, like solar panel installation

FHA Loan Calculator for Illinois

Mortgage calculators can help determine your mortgage payment and break down that payment into individual expenses such as taxes, insurance, and HOA fees. Calculate your monthly mortgage payment for a home in Illinois by inputting your loan term, home price, and down payment into the corresponding box on the mortgage calculator.

In addition to the mortgage calculator, we offer a loan comparison calculator, rent vs. buy calculator, and refinance calculator, among others. Our goal is to provide clients with a full suite of tools so that they may make the most informed decision possible about their home loans.

We can also do this for you, so reach out to our team at The Home Loan Expert now!

Conclusion: Applying for an FHA Loan in Illinois

FHA Loans in Illinois make mortgages more attainable for first-time homebuyers and other prospective buyers that struggle to meet traditional bank loan requirements. Consequently, FHA Loan requirements are easier to fulfill and offer better affordability.

Need some more support buying your first home? Check out the best first-time homebuyer programs in Illinois.

However, if you’re considering an FHA Loan in Illinois, just get started with The Home Loan Expert. Our local team members are always happy to sit down with our clients and offer them personalized support to make their homeownership dreams come true.

Ready to finally buy that dream Ohio home? Contact us today for a consultation!

Glide Support

Glide Support